The data tells the story

The Theory Held Then Broke

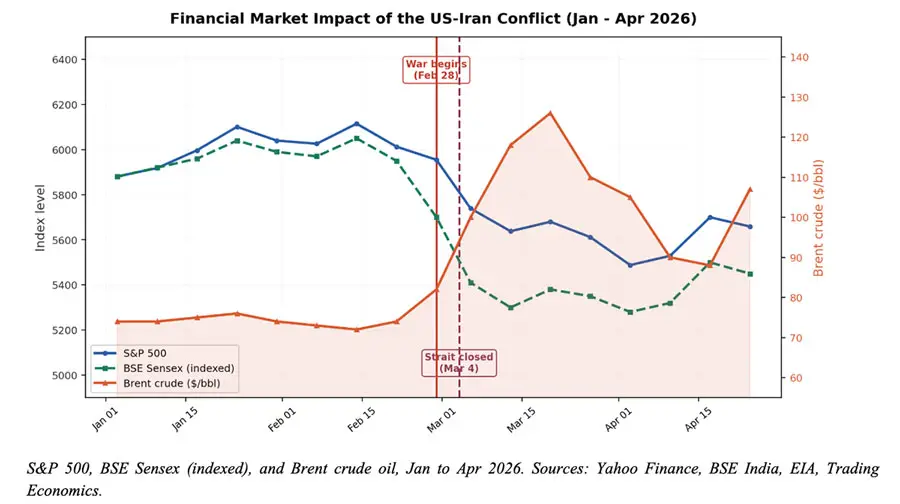

The Efficient Market Hypothesis (Fama, 1970) posits that prices should reflect public information almost instantly. On Day One, they did textbook efficiency. But over the next six weeks, Brent climbed to nearly $128, whipsawed on ceasefire rumors, and crashed 10% on April 17 when Iran declared the strait open only to spike again the next day when Tehran reversed course, and IRGC gunboats fired on vessels attempting transit. Markets can price a shock efficiently. They cannot price a shock whose parameters change by the hour. The EMH works when information is stable. The Hormuz crisis showed what happens when the information itself is contradictory (Caldara & Iacoviello, 2022).

Diversification Failed Where It Was Needed Most

Dynamic connectedness (Diebold & Yilmaz, 2012) explains how this happened. In stable periods, oil, equities, bonds, and currencies respond to their own fundamentals. When the Hormuz closure hit, crude became the dominant transmitter of volatility to every other asset class. The transmission operated through four channels physical supply disruption, inflation expectations, currency depreciation in oil-importing economies, and sectoral rotation within equities all activating within hours, not days. Brent recorded a sharp surge during March, among the most pronounced monthly increases observed in recent periods of market stress. Industry assessments describe this episode as one of the most severe supply disruptions observed in the global oil market in recent decades. Volatility clustered exactly as GARCH models predict (Bollerslev, 1986): wild days arrived in packs, and neither the VIX nor the MOVE index returned to pre-war levels because the core uncertainty remained unresolved.

The key lesson is not that financial theories failed, but that their assumptions were violated. Models such as EMH, MPT, and volatility frameworks remain valid within stable informational and structural environments. What the Hormuz crisis illustrates is the need to explicitly model instability in information, time-varying correlations, and regime shifts. For researchers, this points toward frameworks that allow for dynamic spillovers and structural breaks. For practitioners, it reinforces a simpler insight: in systemic geopolitical shocks, risk is not diversified away; it is redistributed across markets with greater speed and intensity than standard models assume.

References

Bollerslev, T. (1986). Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics, 31(3), 307–327.

Caldara, D. & Iacoviello, M. (2022). Measuring Geopolitical Risk. American Economic Review, 112(4), 1194–1225.

Diebold, F.X. & Yilmaz, K. (2012). Better to Give than to Receive: Predictive Directional Measurement of Volatility Spillovers. International Journal of Forecasting, 28(1), 57–66.

Fama, E.F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, 25(2), 383–417.

Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 7(1), 77–91.

MSCI (2026). A Multi-Asset Playbook for Geopolitical Shocks and Oil Supply Disruption. MSCI Research, March 11.

Taleb, N.N. (2007). The Black Swan: The Impact of the Highly Improbable. Random House.

Data: EIA STEO (April 2026); BSE India; CNBC; Trading Economics; Jefferies India Research; Business Today India (March 30, 2026).